It is not hard to recall John Maynard Keynes suggested contractions are the result of sluggish demand rather than price fluctuations back when both money was indexed to metal and productive capital could be destroyed.

Monetary financing of public deficits coupled with persistent capital depletion (some demand today that zombie firms be retired) during WWII surely proved Keynes right – would applying Keynes today be equally correct?

Surely we do not ignore capital value was determined by its indexing to metal commodities and intermittent capital controls (with corresponding risk premia) when Keynes wrote the General Theory. Should we then ignore the effects low interest rates (thus relative prices) have on exchanges between countries?

Robert Kuttner noticed long ago that the end of Bretton Woods’ metal peg (1971) propelled capital flight to unregulated economies, causing violent swings in nominal terms of both US current and financial accounts.

The rate of transmission of the US policy rate to the current and financial accounts varied through the years before and after Bretton Woods, the Plaza Accord and the Asian financial meltdown, as visible in the chart above.

As such, monetary and fiscal authorities were seldom able to deliver entirely effective demand sustenance (as Keynes suggested was the State’s role) without feedback effects.

Consider the link between the current account and the real interest rate.

Belloc and Gandolfo demonstrated Obstfelt’s and Rogoff’s prediction of an uneven relationship between current account and real interest rate, when import or export trends impacts prices and thus interest rates, or when the price level differential with other markets engages imports instead of domestic production, is actually observable.

Using data for Italy, the authors‘ proof questions the possible effect and reverse effect of monetary policy on the current account, with important implications on the rate of saving and investment – thus on aggregate demand on the long-term.

As theorised by Obstfelt and Rogoff, real interest rate differentials between regions in different moments, visible for instance in cross-border value chains, underpin the positive (negative) co-movements of interest rate and current account as demonstrated by the following.

Empirical analysis

These co-movements are visible in both the US and Eurozone.

Negative co-movement suggests current account effects dominated the real interest rate until the Louvre Accords that halted devaluation of the USD.

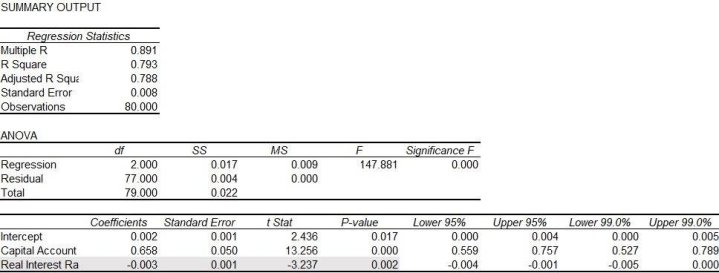

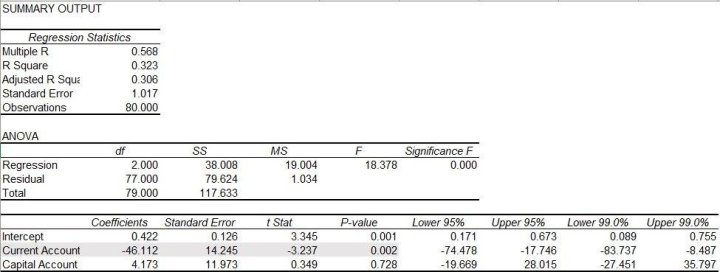

Regressions on the Current Account

Regression on the Real Interest Rate

Regression on the Fed Funds Rate

In the EU, the current account dominates the real interest rate as the negative co-movement implies a decrease in the interest rate occurs in the aftermath of an increase in the current account.

Regressions on the Current Account

Regression on the real interest rate

Regression on the ECB main refinancing rate

The European economy is, on these terms, completely dominated by the Current Account.

As Obstfelt and Rogoff explain, the real interest rate of countries running a current account surplus is below that of foreign counterparts because of expected inflation and the economists’ regression results are complacent with those reported above.

Impact on investment

Two relevant consequences stem from this observation: using monetary policy stimulus to improve EU investment is likely to increase upward pressure on current account surpluses; explicit investment stimulus policies are more effective than low policy rates.

In fact, as lower savings rates correlate with lower investment rates in OECD countries (as remarkably found in work by Feldstein and Orioka), lower ECB policy rates may actually depress investment whilst arguably stimulating consumption.

The comprehensive study of Hausken and Ncube (for sale here, for download here) seems to conclude as much:

“To sum up, the ECB’s unconventional monetary policies are effective, at least in the short run, in preventing a longer period of deflation and a lower level of inflation perception. The simulated effect of the ECB’s QE on the industrial production, unemployment, house prices, consumer confidence, stock markets, and currency exchange, however, are mixed and inconclusive.”

In such circumstance when a stimulus to demand does not entail automatic adjustment of relative real interest rates nor an increase in productive capital – as it did when Keynes wrote the General Theory – perhaps it would be better to explore other stimulus channels.